Career Change for Accountants:

Better-Fit Paths Beyond Traditional Accounting

Many accountants who want a career change are not trying to leave analysis, structure, or business reality behind.

They are trying to leave a narrower pattern inside traditional accounting work.

Often that means some combination of:

- repetitive close cycles

- compliance-heavy rhythm

- audit pressure

- documentation load without enough strategic ownership

- a career ladder that becomes more managerial without becoming more interesting

That distinction matters because "leave accounting" is usually too blunt. A lot of accountants are not rejecting rigor. They are rejecting the exact way rigor gets used in their current path.

That is a much more useful starting point.

The Short Answer

The best career changes for accountants usually preserve something real from accounting while changing the work pattern around it.

That often includes adjacent paths such as:

- FP&A or strategic finance

- finance systems or ERP-adjacent work

- business operations or process improvement

- internal controls, risk, or compliance-adjacent roles

- analytics or reporting-heavy business roles

- implementation, systems, or cross-functional finance operations

The key question is not only "What can an accountant switch into?" It is: which parts of accounting still fit me, and which parts of traditional accounting work are the actual source of friction?

Why Accountants Often Misread The Problem

Accounting compresses a lot of work into one title:

- precision

- control

- documentation

- reconciliation

- interpretation

- policy discipline

- business process visibility

When people burn out or plateau in the field, they often talk as if the only options are:

- stay in accounting

- leave for something totally different

That is usually the wrong split.

An accountant may dislike:

- month-end repetition

- external-audit stress

- the compliance-to-effort ratio

- the distance from decision-making

- highly cyclical workload patterns

without disliking:

- analytical rigor

- structured problem-solving

- understanding how a business really works

- spotting inconsistencies

- building cleaner systems

That is why the first diagnosis has to happen below the title.

What Accounting Usually Trains Better Than Accountants Realize

People outside the field often reduce accountants to bookkeeping or reporting. People inside the field often understate how much wider the training actually is.

Good accountants usually build strength in:

- pattern recognition

- error detection

- process logic

- systems discipline

- translating messy operations into structured records

- understanding what is real in a business versus what is only assumed

- asking where a number came from and whether it should be trusted

Those are durable strengths.

That is one reason adjacent moves often work better than people expect. The strongest transitions are usually built from underlying work patterns, not from title similarity alone. Career-transition and employability research reflects the same basic principle: people move better when they can reinterpret existing capability and connect it to adjacent work rather than treating change like a full reset.[[1]](#ref-1)

What Accountants Often Misdiagnose About Themselves

This is where the search usually gets distorted.

#### “I Only Know Accounting”

This is rarely the full truth.

What is usually true is that the person has spent years using their strengths inside one specific structure of deadlines, controls, and reporting expectations. Once that structure stops fitting, they start mistaking familiarity for identity.

They say:

- I only know close work

- I only know audit support

- I only know technical accounting

But what they often actually know is:

- how to work with incomplete business information and make it usable

- how to identify process weakness early

- how to check whether reality and reporting are diverging

- how to turn messy operational activity into structured evidence

That is a much stronger foundation for an adjacent move than most accountants first assume.

#### “If I Leave Accounting, I Have To Become More Outwardly Strategic”

Not necessarily.

Some accountants do want more strategic or forward-looking work. Others mainly want a healthier operating rhythm, more systems ownership, or fewer cyclical spikes. A better-fit move does not have to become more performative, more presentation-heavy, or more executive-facing just because it sits outside traditional accounting.

Sometimes the right move is not upward in status language. It is sideways into a work pattern that fits better.

#### “Broader Role” Means “Better Role”

This is another trap.

Roles described as broader can still produce:

- shallow reporting cycles

- meeting-heavy coordination

- low control with high accountability

- repetitive support work under a more attractive title

That is why the actual work structure matters more than the prestige of the label.

First Decide What You Want Less Of

This matters more than the title search.

Common patterns include wanting less:

- close-cycle repetition

- technical-accounting depth for its own sake

- audit preparation pressure

- compliance-heavy work with little strategic payoff

- documentation and support work without enough ownership

- highly seasonal workload spikes

Different adjacent paths solve different versions of that problem.

If you skip this step, every finance or operations title starts looking attractive even though the lived work can still feel very different.

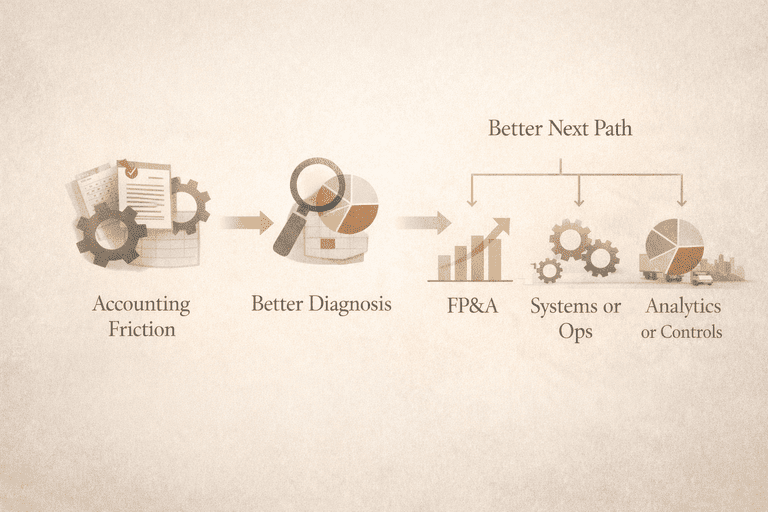

Six Better-Fit Paths Beyond Traditional Accounting

These are not the only options. They are the paths that most often make practical sense because they preserve real accounting strengths while changing the operating model.

1. FP&A Or Strategic Finance

This is often the strongest adjacent move for accountants who still like financial rigor but want to move closer to planning, forecasting, and decision support.

What transfers well:

- comfort with numbers that have to reconcile to reality

- variance thinking

- business-model awareness

- structured analysis

- documentation and logic discipline

What changes:

- more forward-looking work

- more scenario planning

- more stakeholder communication around business decisions

- less pure historical reporting

This path fits best when you still like financial analysis, but want more interpretation and more strategic relevance than traditional accounting gives you.

2. Finance Systems, ERP, Or Systems-Adjacent Roles

Some accountants are strongest not only in accounting logic, but in understanding how accounting processes live inside systems.

That can point toward:

- finance systems

- ERP support or implementation

- systems administration adjacent to finance

- process design and workflow improvement

What transfers well:

- process precision

- control awareness

- understanding why data integrity matters

- ability to spot where systems and reality diverge

- comfort with structured logic and repeatability

What changes:

- less cyclical close ownership

- more cross-functional systems work

- more process and configuration thinking

- more emphasis on usability, workflow, and adoption

This path fits best when you like structure and rigor but want it applied to how work gets built, not only how it gets reported.

3. Business Operations Or Process Improvement

Some accountants eventually realize that what they are best at is not just the financial output. It is understanding how underlying work really happens.

That can make business operations or process-improvement roles surprisingly strong fits.

What transfers well:

- process mapping

- control thinking

- root-cause analysis

- spotting inefficiency and friction

- comfort with structured documentation

What changes:

- less accounting policy focus

- more cross-functional operational ownership

- more continuous process work

- more emphasis on workflow and execution rather than only financial correctness

This path fits best when you want to stay analytical but closer to how the business actually runs.

4. Internal Controls, Risk, Or Compliance-Adjacent Work

This path is not for everyone leaving accounting, because some people are trying to leave control-heavy work, not deepen it.

But it can be a strong move when the accountant still likes:

- controls

- risk thinking

- process integrity

- policy interpretation

- finding where things can go wrong before they do

What changes:

- the frame becomes broader than accounting entries alone

- the work may sit closer to governance, operational risk, or control design

- the day-to-day rhythm may feel more investigative or systems-oriented than close-driven

This path fits best when you still like rigor and safeguard thinking, but want the work to feel less repetitive than traditional accounting cycles.

5. Analytics Or Reporting-Heavy Business Roles

Some accountants want to preserve analysis but move away from accounting identity.

That can point toward:

- business analytics

- reporting and performance analysis

- finance-adjacent data roles

- operational reporting

What transfers well:

- precision

- comfort with data quality

- interpreting what numbers do and do not mean

- structured logic

- skepticism toward weak evidence

What changes:

- more business-question framing

- more presentation and interpretation work

- less formal accounting structure

- more emphasis on insight, not only correctness

This path fits best when you still want analytical work, but want less of it trapped inside traditional accounting outputs.

6. Implementation, Transformation, Or Cross-Functional Finance Operations

Some accountants are strongest when a company is changing something:

- a new system

- a new process

- a cleaner close

- a tighter control environment

- a better cross-functional workflow

That can point toward implementation or transformation-heavy work.

What transfers well:

- detail discipline

- process understanding

- change-impact awareness

- structured communication

- ability to translate between technical requirements and operational reality

What changes:

- less static recurring work

- more project-based or transition-based work

- more collaboration across teams

- more visible influence on how work gets done

This path fits best when you still like finance and systems discipline, but want more movement and change-oriented work.

Common Traps In The Exit Search

This is where accountants can lose time.

“Anything In Finance”

Finance is not one thing.

Some accountants move toward finance because it sounds broader or more strategic. That can be right. It can also be vague. Some finance roles are much more presentation-heavy, relationship-heavy, or ambiguity-heavy than accountants expect. Others preserve almost all of the same pain points with a different label.

The question is not whether the role sits under a broader finance umbrella. The question is whether the work pattern is actually better.

A Higher-Paying Version Of The Same Friction

Sometimes the next obvious move is simply a more senior version of the same structure:

- more close pressure

- more audit responsibility

- more review work

- more people management on top of the same cycle

That can be rational financially. It is not always a fit improvement.

Roles Chosen Only Because They Sound More Strategic

"Strategic" is one of the most misleading career words.

Some roles sound strategic and still involve:

- repetitive reporting

- low decision authority

- heavy stakeholder management without enough ownership

Do not use prestige language as a proxy for better fit.

How To Choose And Validate The Right Path

Once you have two or three likely path families, stop relying on abstract role names and start reading real postings closely.

Look for repeated signals in:

- how much of the work is recurring cycle support versus forward-looking analysis

- whether the role owns systems and process or only reports on them

- how much stakeholder influence is required

- whether success depends on technical rigor, business framing, implementation skill, or presentation skill

- whether the role is closer to operations, finance, systems, or governance

This matters because titles like:

- finance manager

- business analyst

- operations analyst

- finance systems lead

- strategic finance

can describe very different daily lives across different companies.

The title is not enough. The task mix tells the truth.

Use These Fit Filters

At this point, the best question is not which title sounds smartest. It is which part of accounting still feels like yours.

Use these filters.

#### If You Still Like Financial Interpretation, Look Harder At FP&A

This usually fits when you still want:

- analytical rigor

- business context

- planning logic

- structured financial thinking

but want less:

- backward-looking repetition

- close-driven identity

#### If You Like Systems And Process More Than Reporting, Look Harder At Finance Systems or Ops

This usually fits when your strongest instinct is:

- why is this process built this way?

- where does the handoff break?

- how could this system produce cleaner output with less friction?

#### If You Like Controls And Integrity More Than Storytelling, Look Harder At Risk or Controls

This usually fits when rigor and safeguard thinking still feel satisfying, but you want the work to operate at a wider systems level.

#### If You Like Analysis But Want Less Accounting Identity, Look Harder At Analytics

This usually fits when you still want evidence-based work, but not necessarily inside accounting language or accounting cycles.

How To Pressure-Test The Next Role Before You Move

Do not stop at title appeal.

Pressure-test the role against the actual problem.

Ask:

- does the role still revolve around the same monthly or quarterly cycle I am trying to leave?

- does it increase stakeholder influence in a way I actually want, or just add more meetings?

- does it preserve the analytical strengths I value, or only the endurance I developed?

- does it move me closer to work I want more of, or only away from the current pain?

This matters because adjacent roles can still hide the same pattern under cleaner language.

What A Strong Accountant Exit Usually Preserves

The best adjacent move usually preserves at least one of these:

- analytical rigor

- process logic

- skepticism about weak evidence

- comfort with systems and controls

- understanding how operations become numbers

If the next role uses almost none of that, the move may still be right, but it is no longer a simple adjacent transition. It becomes a larger reset with a different risk profile.

How To Explain The Move So It Sounds Coherent

Accountants often undersell themselves here by making the move sound too vague.

Weak version:

- I want to do something more strategic

- I want to get out of accounting

- I am looking for a broader business role

Stronger version:

- Accounting gave me strong rigor around process, controls, and understanding how numbers connect to business reality. Over time I realized I want to use that strength in a more forward-looking and decision-support context, which is why FP&A is a more fitting next step.

Or:

- My background in accounting built strong systems discipline and the ability to spot where process and reporting break down. That is why finance systems and workflow improvement feel like a stronger fit for me than staying in a traditional close-focused role.

That kind of explanation preserves continuity while making the next move sound deliberate.

Final Answer

The best career change for an accountant is usually not a random escape from numbers. It is a better-fit path that preserves real strengths from accounting while changing the work pattern that stopped fitting.

Once you separate what accounting trained you to do from the specific rhythm of traditional accounting work, the options get much clearer. You are no longer asking what unrelated role you could possibly force yourself into. You are asking where analytical rigor, process judgment, and business discipline can be used in a way that fits you better now.

References

[1] De Vos, A., et al. Career transitions and employability. Journal of Vocational Behavior, 2021. https://www.sciencedirect.com/science/article/pii/S0001879120301007

[2] ONET OnLine. Advanced Search*. https://www.onetonline.org/help/online/advanced

[3] ONET OnLine. Summary Report and Occupation Structure Resources*. https://www.onetonline.org/

[4] Fugate, Mel, Angelo J. Kinicki, and Blake E. Ashforth. Employability: A Psycho-Social Construct, Its Dimensions, and Applications. Journal of Vocational Behavior, 2004.

[5] OECD. Career Guidance for Adults in a Changing World of Work. https://www.oecd.org/en/publications/career-guidance-for-adults-in-a-changing-world-of-work_9a94bfad-en.html

[6] Savickas, Mark L., and Erik J. Porfeli. Career Adapt-Abilities Scale: Construction, Reliability, and Measurement Equivalence Across 13 Countries. Journal of Vocational Behavior, 2012.

[7] U.S. Bureau of Labor Statistics. Accountants and Auditors. https://www.bls.gov/ooh/business-and-financial/accountants-and-auditors.htm

[8] CareerMeasure. Methodology. https://careermeasure.com/methodology

See Your Stronger-Fit Next Moves

Get a clearer picture of which adjacent paths fit you better before making a bigger jump.

Builds CareerMeasure hands on and writes about career fit, role transitions, and the gap between generic personality advice and evidence-based career decisions.

Community Discussion

Share your thoughts about this article

Delete Comment?

Are you sure you want to delete this comment? This action cannot be undone.